Store Credit Innovation

Innovating store credit transactions at self-checkout

Winter 2019:

12/30/2019

The Problem

Labor is typically limited in stores,

everytime a customer has to wait

on an associate for help, it creates

a potential bottleneck within the

process. Especially at higher

volume stores.

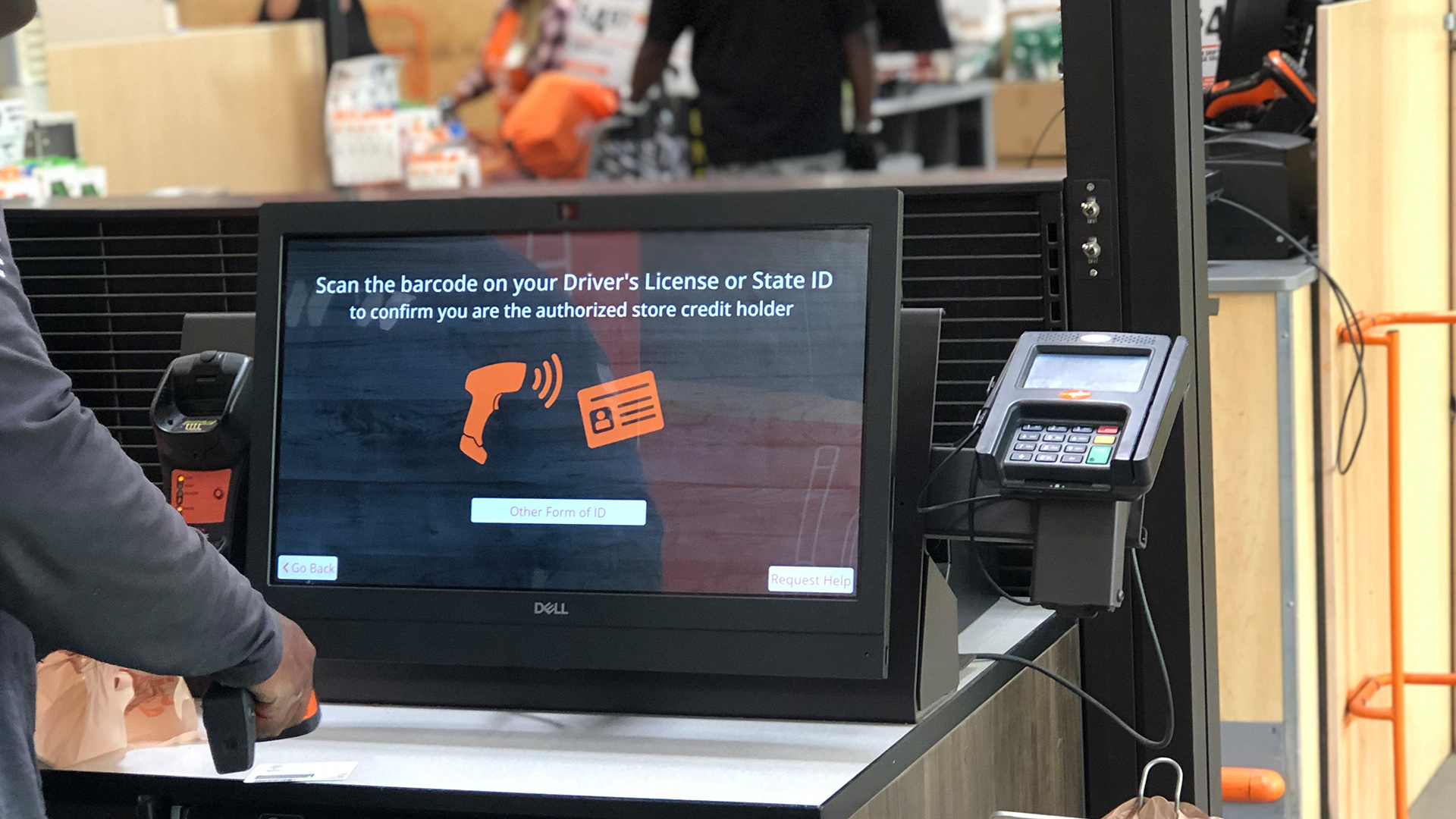

The purpose of the SCID (Store Credit ID) Initiative is to reduce the amount of *interventions at Self-Checkout.

*(the amount of times cashiers have to intervene to solve a customer issue)

Every preventable intervention at self checkout has a series of detrimental impacts on the User Experience:

- Slower Lines

- Associate Overload

- *Shrink

*illicit activities

The Hypothesis

By allowing customers to scan

their own ID to redeem store

credit, we can reduce friction at

self-checkout, increase checkout

speed, and reduce associate labor

load.

Benefits:

By allowing the customer to scan their own ID to redeem store credit, we can accomplish the following benefits:

- Improve checkout speed

- Decrease associate hassle

- Reduce and/or remove customer wait time

Risk Factors:

- Due to the variance in ID images across the country, the generic License/ID image may be misinterpreted by customers.

- Frustration may ensue for family members or married couples who attempt to share store credit

- Customers may be concerned about their privacy

- Customers may not be confident about the new protocol

The Big Test

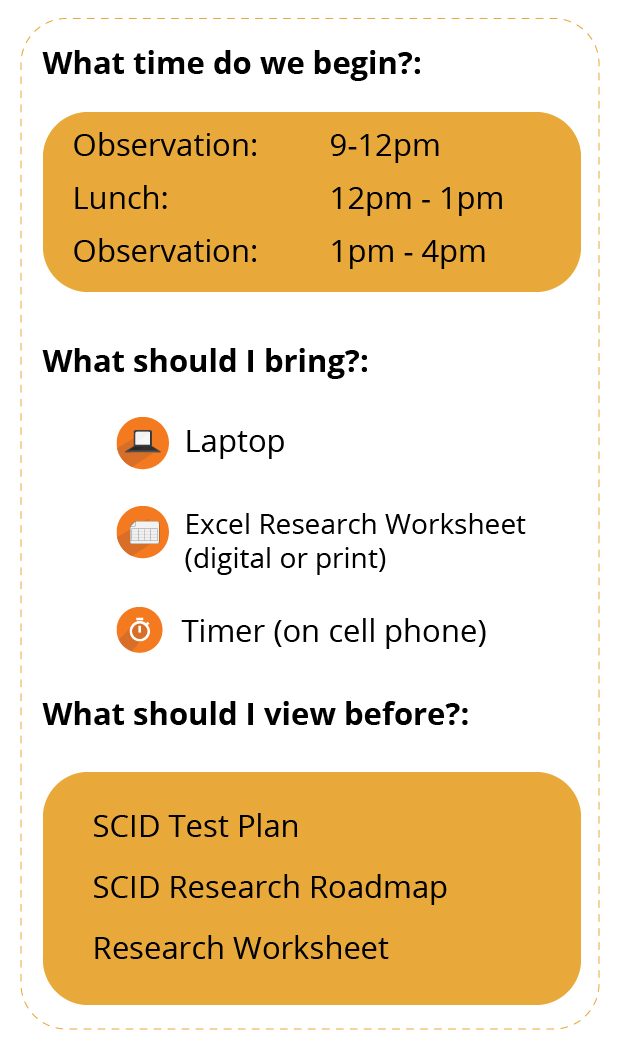

The test was comprised of a series of studies, both in-state and out-of-state.

Research was set to span from the morning, until the latter parts of the evening. Each recruit was equipped with a laption, a research worksheet, a timer and a series of chargers to help us keep all of our equipment charged and ready.

Test Plan Details

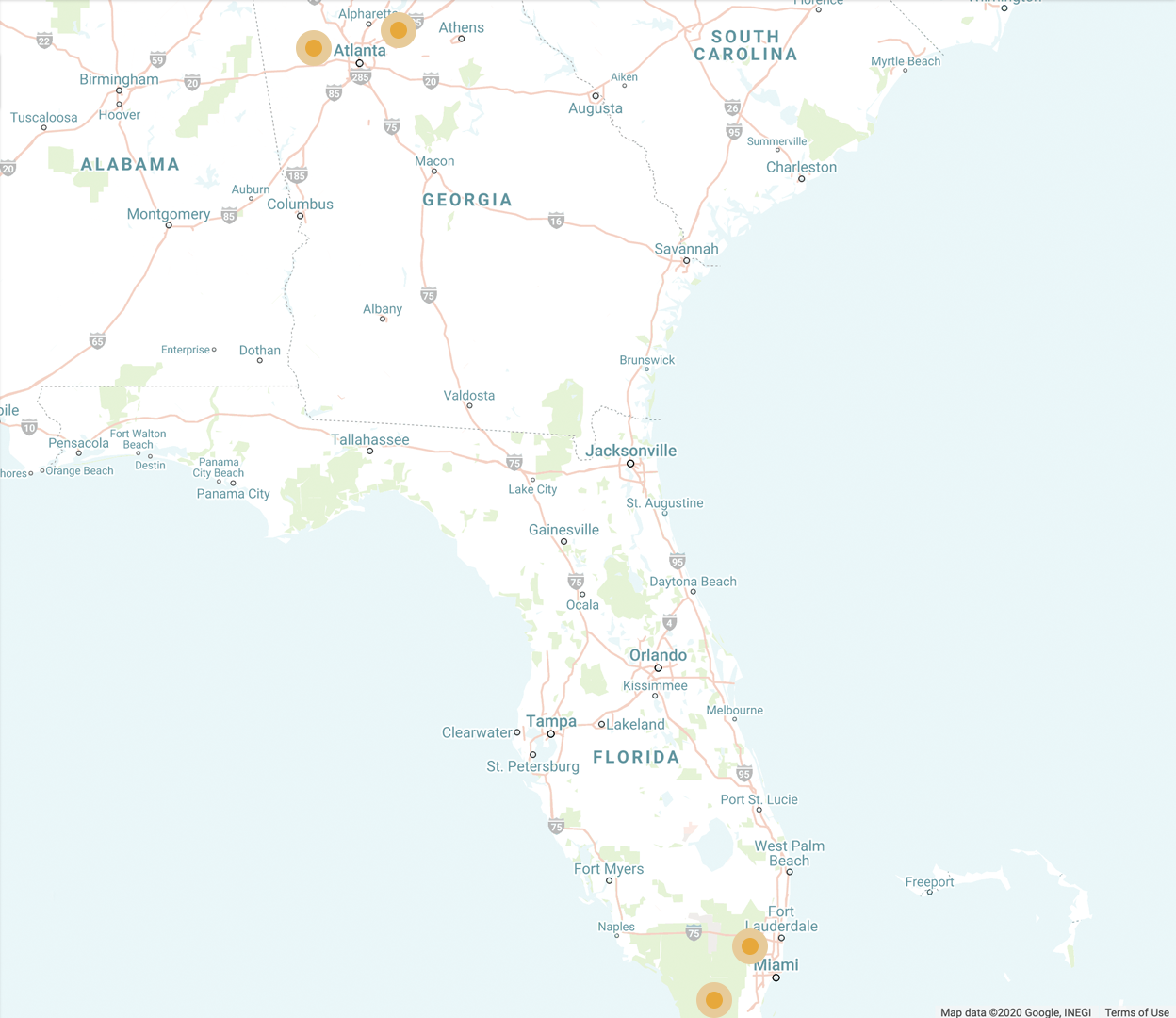

Where we went

Locations

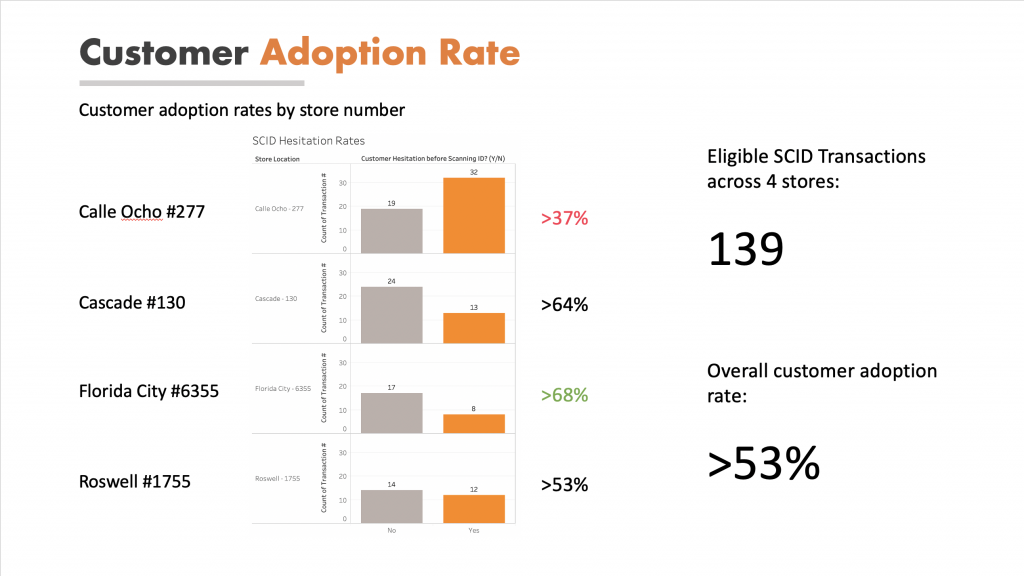

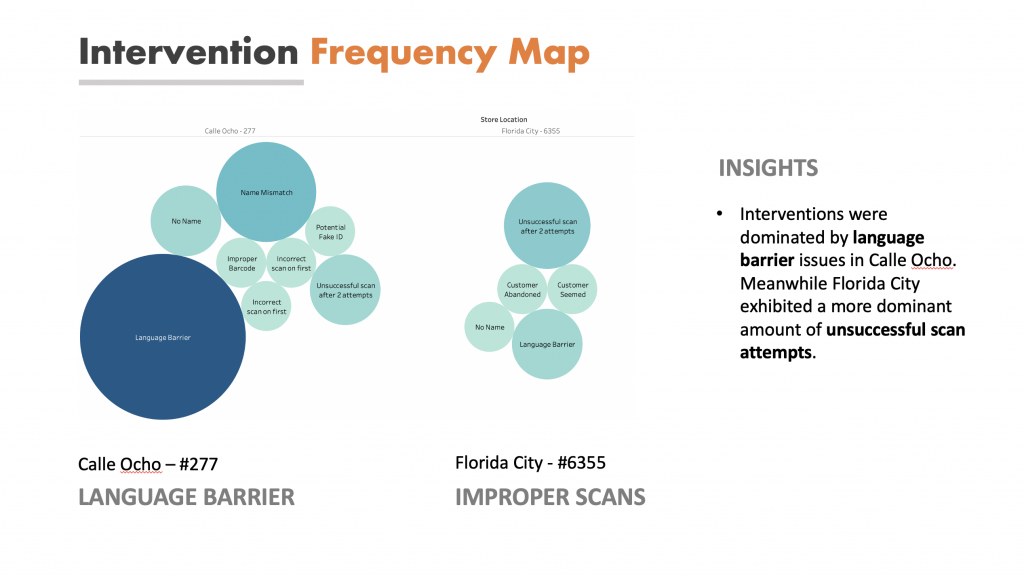

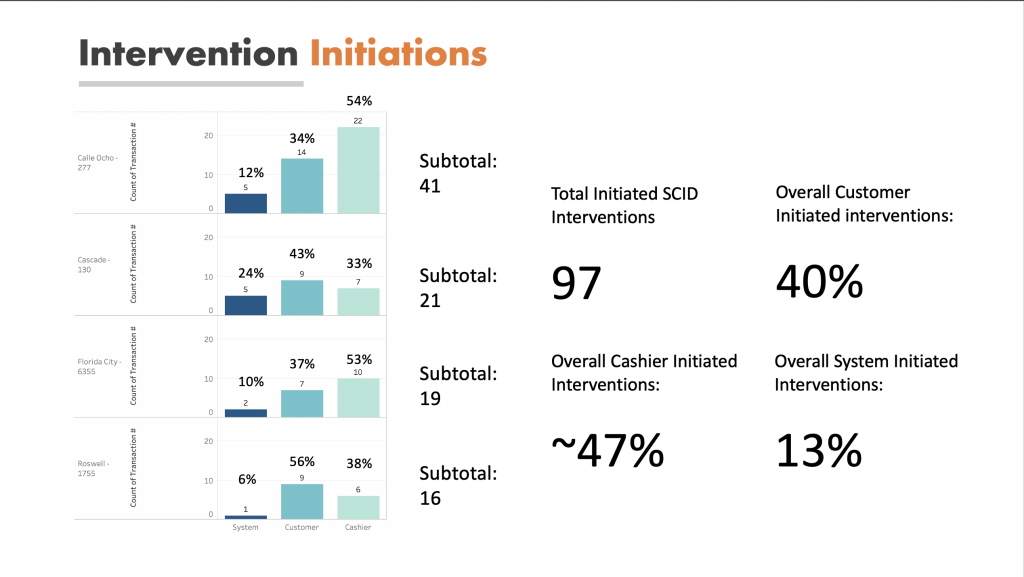

Calle Ocho FL

Florida City FL

Buckhead GA

Roswell GA

Who We Brought

Participants

1 User Experience Designer

1 Software Engineer

1 Product Manager

1 Store Ops Specialist

1 Senior Designer

4 Observational Volunteers

4 Field Captains

How We Did It

Method

6 week pilot

4 weeks of observations

2 weeks of interviews (Week 1 and Week 6)

Research Budget: $3521

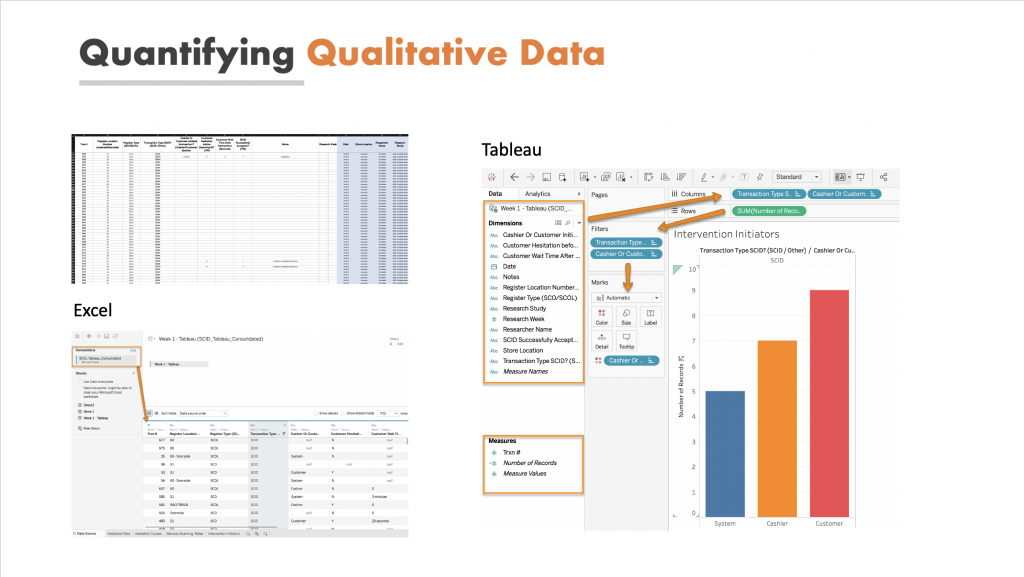

Note: Additional Quantitative data was gathered to support this

Qualitative Research Effort

Measurements

Qualitative

Intervention Initiation

Who initiated the intervention? Cashier or

Customer?

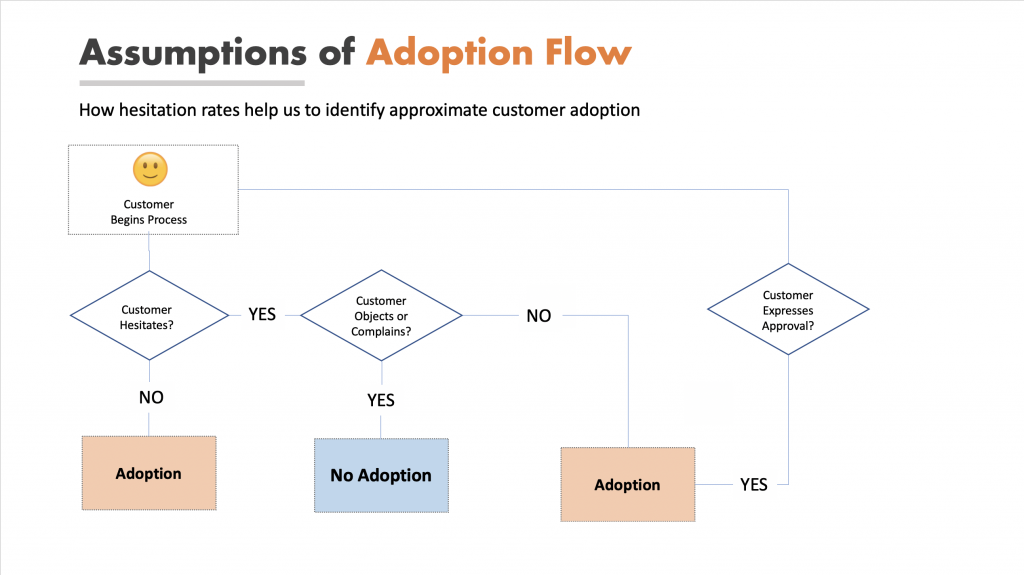

Hesitation Rates

Did the customer *hesitate before Scanning

ID?

Adoption Rates

Customer vs. Associate Adoption of the new

protocol

Technical

Technical Considerations

Was the SCID successfully applied? Why or

why not?

Transaction Detail

What was the customer wait time post

intervention?

Quantitative

Systematic Data

Register #

Request Help Usage

Intervention count (amount and location)

Transaction checkout time

Key Takeaways

- Most customers were not concerned about privacy (not expected)

- Associates in english speaking stores were generally confident in customer’s ability to succeed (not expected)

- Associates in spanish speaking stores were less confident in customer’s ability to succeed without assistance

- Generic SCID visual wasn’t a major hindrance, although, it was a notable inconvenience for customers who had out of state IDs

- The new system was cumbersome for family members who tend to share last names and Store Credit

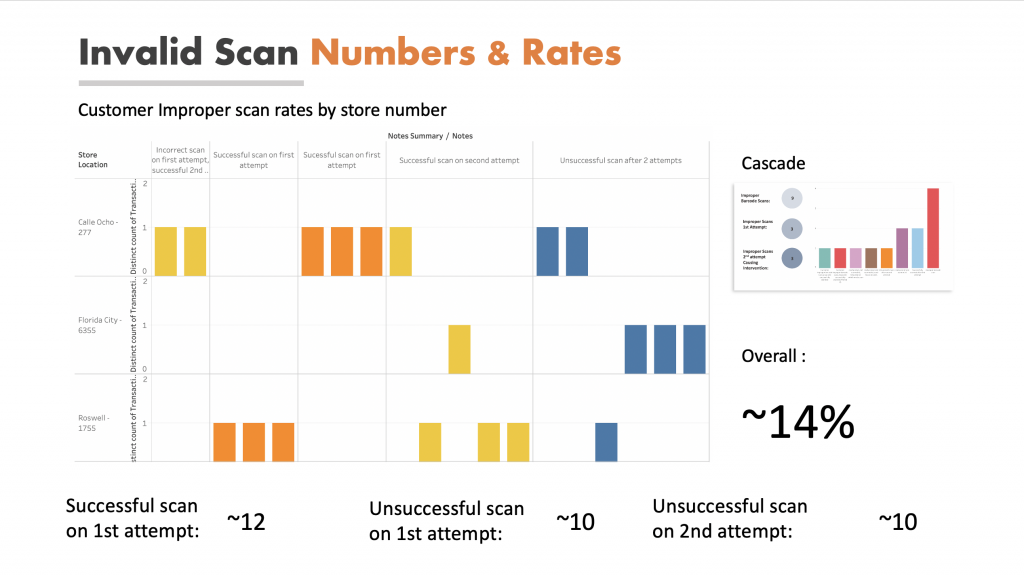

- Since IDs have 2 barcodes, the image leveraged was generally not descriptive enough to convey which barcode needed to be scanned

Updates based on findings

- Update image to reflect more descriptive instructions if customers don’t scan correctly the first time